By Guest blogger - Matt Walker, Chief Analyst, MTN Consulting

If you’re selling technology to communications operators and automation isn’t front and center in your messaging, then you aren’t reading the room right.

Automation is viewed as not only bringing cost savings, but also adding intelligence that humans alone cannot deliver. That applies to deploying and troubleshooting services; designing, building and operating networks; and, even back in the factory & lab setting.

The Automation Topic Is Coming Up Throughout OFC 2021

On June 6, for instance, a lab automation hackathon was held, as was a workshop on “Cognitive Network Automation: How Smart Can Optical Transport Networks Be?”. The latter featured contributions from vendors, operators, and academics. But automation is a broad topic which is finding its way into many discussions. Some relate to individual parts of the network, such as the data center or fiber access network or customer premises, or entire layers of the network, or specific network functions. Nearly every vendor selling to operators recognizes the customer need for automation, as their customers (especially the telcos) attempt to do more with less. In Ciena’s earnings call last week, for instance, CEO Gary Smith called out “strong underlying secular demand for bandwidth and automation” as central drivers for its business.

Automation is Key to Many Vendor Wins

Over the last several months, many OFC participants have announced automation-related wins; a few of the many examples:

-

Viavi Solutions announced a new optical spectrum analysis module, the MAP (multiple application module) mOSA. The mOSA module is an enhancement to Viavi’s testing portfolio. Viavi VP Tom Fawcett says that the module “delivers unmatched scalability, efficiency and precision to meet escalating demands for optical manufacturing testing.” (June 2021)

-

Netcracker (NEC): greenfield mobile operator DISH is using a full-stack digital solution for its interaction with transport providers, covering “customer order management, customer contract management, billing management, resource management, service management and orchestration.” (April 2021)

Each of the above vendors have many similar deployments, and most other vendors have solutions where automation plays a key role. In addition, quite a few operators are spending heavily on internal R&D to better automate processes; that includes cable companies like Cox and Comcast, large integrated providers like AT&T, and mobile-centric telcos like Vodafone. Webscale players like Google, Facebook, and Microsoft made automation central to their operations from the start. Google’s “Zero Touch Network” concept is illustrative. All three of these companies, notably, are speaking at OFC 2021.

Running a network composed largely of enormous data centers linked up with ultra-high capacity transport fiber links – mostly built in the last 5-10 years – is a bit simpler than what a typical telco faces. Telcos face flat revenues, and must deliver a wide range of services to diverse end markets, over complex networks, built over generations. That’s why the automation opportunity appears so much larger, even if more challenging, in the telco environment.

Telcos Are Learning How To Slim Down — Automation a Factor

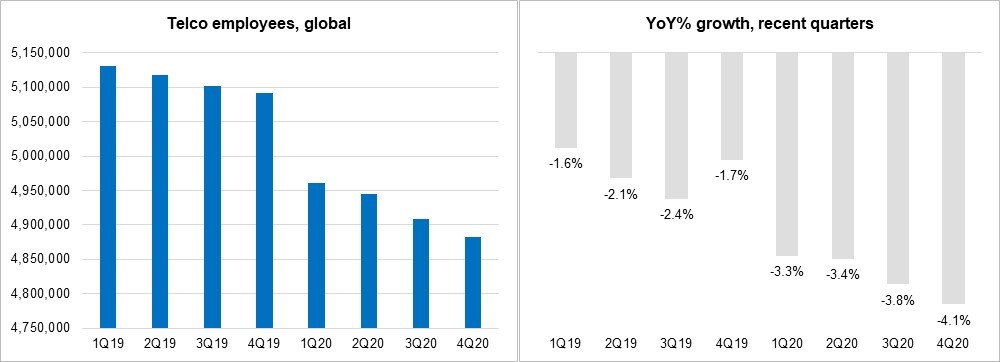

Telecom operators, aka telcos, had a rough year in 2020 if you consider their top line only. Revenues dropped 1.1% to $1,794 billion. That decline is roughly the same as 2019. Surprisingly, telco profitability improved in 2020. For the 138 telcos MTN Consulting tracks, EBITDA margin averaged out to 34.5%, higher than 2019’s average of 32.8%, and in fact higher than at any point in the 10 years we’ve tracked the sector. EBIT (operating) margin was also strong, 14.9% in 2020 and the highest in 6 years. Debt continues to be an issue for some telcos, and a few are selling assets to improve their position, but earnings were surprisingly solid.

There are many reasons for 2020’s improved profitability. One clear factor, though, is that telcos are getting serious about reducing their headcount and implementing automation across their operations. In 2020, telco headcount fell 4% to below 5 million (figure).

Source: MTN Consulting

That doesn’t necessarily mean telcos are spending less on their workforce. In fact, labor costs as a share of telco opex (excluding depreciation & amortization) rose in 2020, from 23.6% in 2019 to 24.0%. The average employee is getting pricier as hard-to-get software skills become crucial for hiring.

Automating network functions is not a new thing, but is accelerating due to telcos’ ongoing business needs and improved vendor capabilities. Many telcos reference their efforts to automate in earnings reports. Just one example: Orange’s latest annual report notes that “digital acceleration” of the customer experience is a priority, and the automation of network management and maintenance is a central part of its “Scale-Up” operational efficiency program. The French telco adds that artificial intelligence algorithms make it possible to automate and optimize things like detecting the cause of a fiber failure, or automatically adjust mobile capacity with fluctuations in traffic volumes during the day. At OFC 2021, Orange makes several appearances, including a session held on June 7 on “Operationalizing Partially Disaggregated Optical Networks.”

Vendors and Automation

Vendors such as those cited earlier (Ciena, Netcracker/NEC, and Nokia), and many others, have embraced automation as a selling point across their portfolio. The ability to deliver this has also motivated some recent acquisitions. In May, Cisco acquired Sedona Networks, known for its NetFusion product which – per the company – “automatically discovers, aggregates and analyzes network data from multiple online systems, optical and IP sources, providing a unified, real-time and accurate network-wide data model.” Juniper unveiled its Paragon automation portfolio earlier this year, based in part on a series of acquisitions in the space (Netrounds, 128 Technology, and Apstra). Paragon includes five tools, four from Juniper and one from a partner, aimed at allowing telcos to model and test new services, then automatically deploy and monitor them once live, solving problems with minimal human intervention.

The need for network automation seems likely to inspire both M&A transactions and OFC sessions for years to come.

MTN Consulting

Posted: 9 June 2021 by

Guest blogger - Matt Walker, Chief Analyst, MTN Consulting

| with 0 comments