By Jeff Heynen, Dell'Oro Group

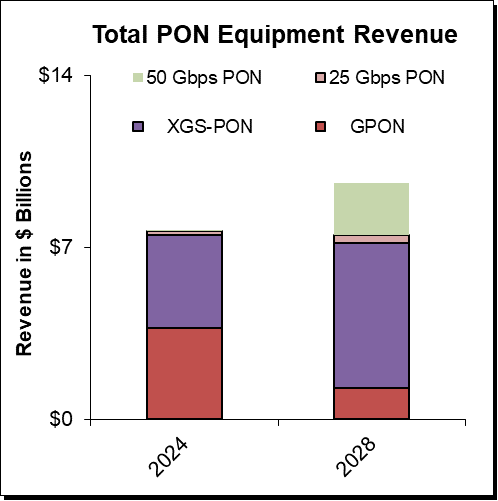

After five straight years of revenue growth from 2018 to 2022, 2023 witnessed an overall decline in PON equipment revenue, as service providers focused on reducing their equipment inventories they had built up in 2022, thereby ending a period of fiber network expansion that was further catalyzed by both public and private capital. Within this five-year span, total PON equipment revenue doubled, jumping from $6B globally in 2018 to a peak of $12B in 2022.

Within that time frame, fiber broadband expansion also became a global phenomenon, not just limited to China and the Asia-Pacific market in general. In fact, from 2018 to 2022, China’s share of PON equipment revenue declined from 56.3% to 39.8%. Meanwhile, North America’s revenue share increased from 12.6% to 16.4%, while EMEA’s share increased from 13.7% to 20.4%.

We anticipate those geographic share shifts will accelerate beginning in 2025, partially thanks to the pending $42.5B BEAD (Broadband Equity, Access, and Deployment) program in the US, but also due to a renewed construction phase for many larger tier 1 operators. Underlying this re-invigoration of the market will be a steady increase in fiber network valuations, an increase in the available labor, and a reduction in overall input costs. Further, we expect service providers will prioritize aerial and shallow dig builds in the short term to more cost-effectively achieve stated homes passed goals. These factors should continue to propel the overall PON equipment market through the end of the decade.

Until 2025, however, we do anticipate tier 1 operators continuing to slow their PON equipment purchases through the first half of 2024, as they continue to deplete their elevated inventory levels from last year. But while the tier 1s slow, there will be no slowing the continued efforts by tier 2 and tier 3 operators in both North America and Europe to both upgrade and expand their fiber networks. In fact, the same dynamic that played out in North America in 2023 will likely repeat in 2024, as tier 2, tier 3, utilities, municipalities, and co-ops all continue their buildouts, some subsidized through existing Federal programs, including the Capital Projects Fund, Rural Digital Opportunity Fund (RDOF), the Tribal Broadband Connectivity Program, as well as individual State programs to expand availability to rural and underserved markets.

Meanwhile, in Europe, Deutsche Telekom continues to expand its FTTH network, having achieved its goal of passing nearly 8 million homes at the end of 2023, with a further goal of passing an additional 2.5 million homes in 2024. Openreach in the UK has passed nearly 12 million homes with over 3 million homes now taking the full fiber service.

In Latin America, the transition to fiber is in full swing among nearly all of the region’s operators—including cable operators. Fiber subscribers now exceed cable broadband subscribers, with major operators like America Movil, Telefonica, Oi, and Telmex leading the charge. But large cable operators in the region are also expanding with fiber, using GPON in new builds while maintaining DOCSIS in their existing footprint. Operators including Liberty Latin America, Megacble, Millicom, and Telecom Argentina are all following this path, as they seek to stay ahead of the incumbent telcos, as well as smaller FTTH ISPs that have increasingly popped up in Brazil and Mexico.

Finally, in China, Fiber to the Room (FTTR) is all the rage among the major operators. As its name implies, FTTR deployments involve running fiber along residential baseboards and walls, connecting them to individual ONT Access Points located in rooms within the home, rather than terminating the fiber at a single ONT, which is then connected to a separate gateway for Wi-Fi distribution via Ethernet. Because most of these deployments use XG-PON, the stated goal is to deliver up to a full 10 Gbps of bandwidth throughout the entire home.

For Chinese operators, who are seeing a decline in net new subscriber additions, FTTR serves as a solution not only for technical issues but also as an opportunity to establish a longer-term customer relationship. Most FTTR contracts require an upfront deposit and a 2-year contract, which is relatively novel for fixed broadband in China. From an equipment perspective, FTTR deployments, which average 2-3 ONTs per home, should push spending on ONTs up, even while new OLT port purchases continue to bottom out.

Open Access Networks Take Hold in New Markets

Beyond the traditional service providers, both North America and Europe are seeing a significant increase in the number of fiber joint ventures, as well as open access networks. The rise in both reflects the inherent value of owning fiber-based communications infrastructure, as well as a growing and dynamic marketplace for the dividing responsibilities between infrastructure owners and ISPs. Joint ventures distribute upfront capital costs across multiple organizations, thereby reducing the risk of lower-than-expected take rates and slower return on investment (ROI). Additionally, joint ventures like Gigapower, a partnership between AT&T and asset management firm BlackRock, allow AT&T to provide wholesale open access fiber in AT&T’s out-of-market regions while also granting AT&T ISP access in those regions as the primary tenant.

With labor shortages still delaying numerous FTTH network buildouts, open access networks provide the benefit of allowing multiple ISPs to share the costs of infrastructure, while also being less disruptive to homeowners and municipalities since only one operator is trenching fiber. For these reasons, we expect to see additional open access networks expand their footprints, helping target communities achieve homes passed goals in more reasonable timeframes.

Additionally, open access networks are giving service providers of all stripes the ability to become fixed broadband providers, as the importance of broadband connectivity is only growing and the ability for ISPs to have flexibility in how they deliver broadband services is also only growing.

A notable example of this trend is T-Mobile in the US. T-Mobile has pioneered in the 5G Fixed Wireless Access (FWA) market for residential broadband service, racking up a 4.8 million cumulative broadband subscribers through the end of 2023. The operator has disrupted traditional fixed broadband players, particularly cable operators, whose subscriber growth has stalled, largely attributed to T-Mobile’s success in offering a lower-priced residential broadband service.

Nevertheless, T-Mobile does have finite capacity in many markets, limiting the number of FWA subscribers it can support. But the operator certainly doesn’t want to cede the ground it has won. Therefore, the operator has partnered with companies providing open access fiber networks, including Tillman FiberCo, SiFi Networks, Intrepid Networks, and Pilot Network, to offer their own T-Mobile-branded Fiber-to-the-Home (FTTH) service to subscribers.

Over time, we anticipate T-Mobile expanding its open access fiber partnerships and the total number of markets it serves, especially in the latter part of this decade as a wave of consolidation is expected to occur so smaller operators can achieve economies of scale.

XGS-PON to Lead the Way Through the End of the Decade

The technology beneficiary of all these deployments and expansions will be XGS-PON, which already surpassed 2.5 Gbps GPON revenue back in 2022, but will more than double it in 2024. We see more scenarios now in which service providers rely on XGS-PON to deliver broadband to the vast majority of their residential subscribers. Additionally, they layer on 25GS-PON to offer premium tiers of 10Gbps or more, as well as enterprise connectivity, all at just a small incremental increase in cost.

With average annual growth rates in bandwidth consumption returning to more normal, pre-pandemic levels, the need to dramatically increase billboard speeds has become less pressing. Instead, the focus for service providers now is how to maximize their access infrastructure investments to flatten the network, address more use cases and market segments, while also building sustainable networks that consume less power than their predecessors.

Because of our more normalized expectations for bandwidth growth, along with conversations with both equipment vendors and service providers, we have reduced our short-term forecasts for 50G-PON, pushing out the ramp in adoption from 2026 to 2028. Although early deployments of asymmetric 50/25 PON are expected, primarily in China, work to define the specification for symmetric 50G-PON is still underway. Symmetric speeds are what service providers want to deploy going forward, so the vast majority of those considering 50G-PON as their next step will likely have to wait until at least 2026 for product availability.

In the interim, whether deployed alongside GPON in combo environments or in standalone configurations, XGS-PON will serve as the workhorse technology for large-scale residential deployments through 2030, if not beyond.

About Jeff Heynen

Jeff Heynen joined Dell’Oro Group in 2018. Mr. Heynen brings over a decade’s worth of experience in both fixed and wireless broadband technology and market analysis and consulting. With Dell’Oro Group, Mr. Heynen will lead the Broadband Access and Home Networking market research, which encompasses cable, fiber, copper, and emerging wireless broadband technologies and trends. Additionally, Mr. Heynen will help shape coverage of next-generation broadband access architectures and service models.

Posted: 14 February 2024 by

Jeff Heynen, Dell'Oro Group

| with 0 comments