By Julie Kunstler, Chief Analyst, Broadband Access Intelligence Service

The large PON forecast, and it could be larger

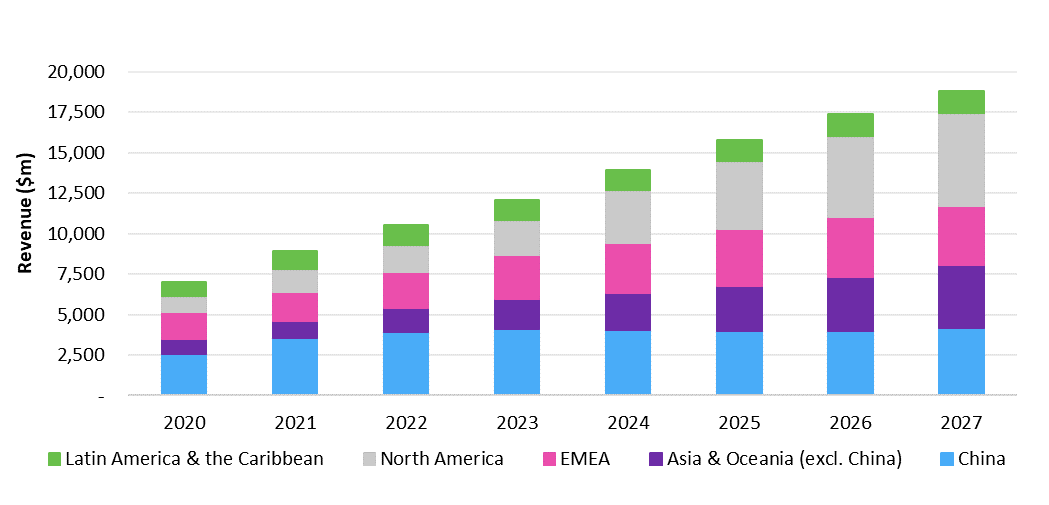

The PON equipment forecast is expected to exceed $18bn in 2027, as shown in Figure 1. Please note that this current forecast reflects supply constraints impacting the FTTP market. Despite the supply constraints, the consumption of PON equipment market will grow, and while China’s consumption of PON equipment remains robust, it is no longer the dominating force behind the strong forecast.

![]()

There are numerous forecast drivers, including:

- FTTP infrastructure builds are gaining momentum in most countries, with the global FTTH household penetration forecast exceeding 1.2 billion subscriptions in 2027.

- Ever-increasing bandwidth demand is the key driver for fiber access, along with demand for low-latency, reduced jitter, and improved quality of experience (QoE). The average household broadband speed is forecast to reach 844 Mbps compared to 121 Mbps in 2020.

- Hybrid working and learning environments will continue.

- Bandwidth demand is growing for enterprises, governments, and vertical industries, including healthcare, banking, transportation, energy and utilities, and manufacturing.

- Consumers and non-consumers are moving to cloud-based applications. Cloud-based applications require bandwidth, along with reduced latency and jitter.

- Cellular traffic will reach 3.4bn TB in 2027, compared to just under 600m TB in 2020. Cellular traffic requires xHaul transport, and fiber-based access is key, with PON playing a small but essential role.

- Many governments support broadband initiatives, treating broadband connectivity as a necessary utility, equating its importance to water and electricity.

Emerging markets add fuel to the PON equipment forecast

Omdia is tracking the strong potential for profitable FTTP rollouts in emerging markets. The costs per premises passed are low, and the willingness to pay is high. Emerging markets represent a substantial market opportunity for PON component and equipment vendors.

There are several key reasons why FTTP is profitable in emerging markets:

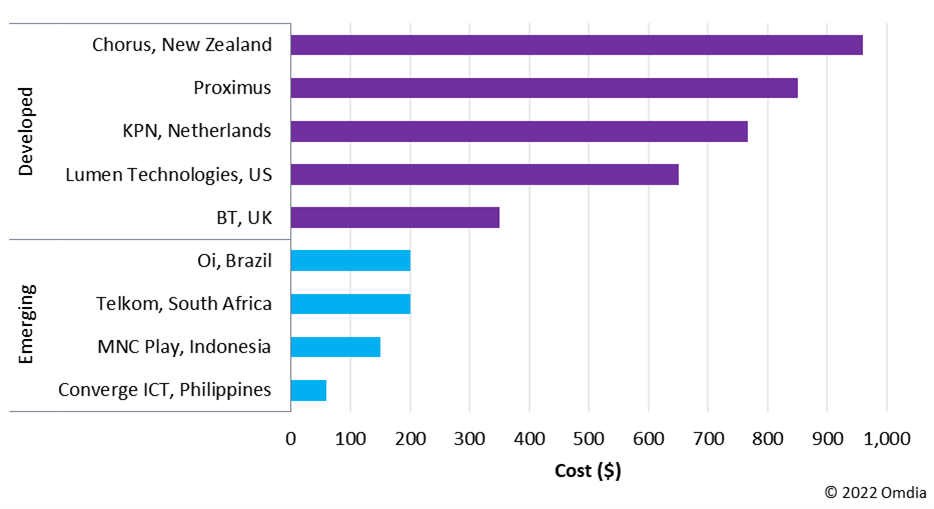

- Low labor costs, high urban population density in emerging markets, and the ability to deploy fiber aerially all push down FTTP costs per premises passed to levels that can be several times below those in developed markets. In many emerging markets, costs per premises passed for FTTP can be around $100‒200 compared with $300‒1,000 in developed markets. Selected cost comparisons are shown in Figure 2.

- Demand for decent quality, uncapped FTTP broadband in emerging markets is robust. Evidence from different emerging markets suggests that households are willing to pay around 4‒6% of their income on an uncapped, decent-quality FTTP connection. This helps to explain why many early FTTP rollouts in emerging markets have seen strong.

- Governments also have a role to play in helping drive the availability of FTTP. Some emerging markets with high FTTP coverage and household broadband penetration have achieved this partly through developing national broadband plans and government investment.

It is worth noting that while FWA may have lower initial costs per home passed than FTTP, it will require future cellular network upgrades as traffic increases. FWA 5G customer premises equipment (CPE) costs are much higher than FTTP ONT costs. All this evidence points to attractive supply-side conditions for FTTP rollouts in emerging markets.

Figure 2: Selected emerging- and developed-market operators, FTTP costs per premises passed

10G and Beyond

10G and Beyond

XGS-PON deployments have rapidly gathered pace. Omdia forecasts that XGS-PON ports will make up the majority (59%) of PON OLT port shipments in North America in 2022, while the figure will stand at around 42% in Western Europe. This reflects the fact that some large US operators are now deploying only XGS-PON for their new rollouts.

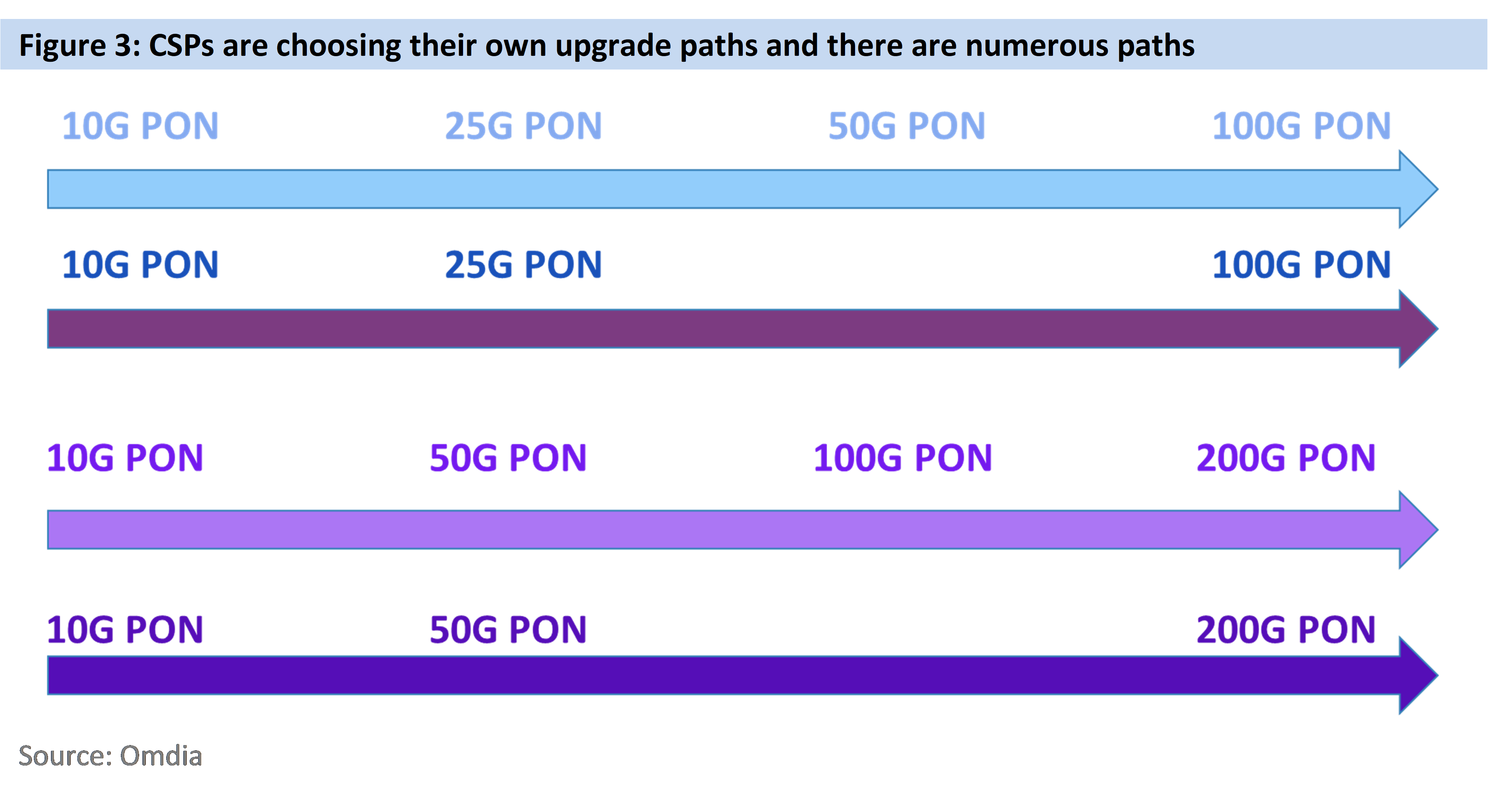

The PON upgrade roadmap reflects the diversity of options for CSPs to choose from as they look to what comes after XGS-PON. Figure 3 summarizes Omdia’s view of the multiple upgrade paths that have emerged and that are likely to occur over time.

For example, 25G GPON is establishing momentum among CSPs in several regions. There will also be opportunities for 50G GPON, especially with network slicing capabilities. In June 2022, one major vendor demonstrated 100G GPON over a single wavelength.

There has been considerable industry debate around 25G PON versus 50G PON. In Omdia’s view, both 25G PON and 50G PON will exist and prosper. They will be adopted by CSPs, based on their respective fiber-access strategies and end-customer requirements.

These developments are significant because they will make it increasingly difficult for FWA and cable to remain competitive in areas with FTTP coverage. DOCSIS 4.0 only supports speeds of up to 10Gbps on the downstream and 6Gbps on the upstream, and this explains why some major cable operators are now upgrading to full fiber.

Beyond Residential – focus on enterprises

While PON’s heritage was “best-efforts,” some operators have been using PON infrastructure to support business customers for more than 15 years. Often these early adopters were smaller operators with single engineering teams supporting network design and equipment choices for different types of subscribers. More recently, new operators, such as AltNets, are using PON infrastructure for multiple types of subscribers. Today, many different types of CSPs are extending PON’s usage to support enterprises.

For many CSPs, the goal is to use the same ODN for residential and enterprise customers, enabling faster RoI (Return on Investment) from accruing more revenues while lowering operating costs. This ODN reuse is sometimes referred to as converged access networking or universal access.

Many CSPs are keen to extend the benefits of PON-based fiber access networks to business subscribers versus the use of P2P. A P2P optical networking solution, such as Active Ethernet, requires a dedicated optical link per subscriber. This approach is expensive in terms of optics and fiber-cabling, and it also poses space and power challenges, especially in dense areas such as cities and towns.

PON networks are well-positioned to meet enterprises continuing bandwidth requirements. XGS PON is widely deployed today, and 25G PON solutions are commercially available. 50G PON has been standardized, and initial deployments are expected in 2024 or 2025. In addition, 100G PON research and development efforts are underway.

PON technologies have evolved to meet many requirements of enterprise services, including:

- SLAs - CSPs are supporting SLAs on PON as they would on P2P fiber. The underlying fiber-based topology does not impact an operator’s ability to provide and meet data throughput, latency, jitter, packet-loss, and redundancy requirements. Moreover, SLAs also encompass time-to-repair metrics, which is why enterprises are prepared to pay higher prices than non-enterprise customers. Importantly the time-to-repair metric is likely to be unaffected by the underlying P2P or PON fiber topology.

- Security - PON technology and equipment solutions contain features that separate, encrypt, and secure data. Features include user isolation, traffic encryption, user activation, and message integrity.

- Redundancy - PON networks can provide redundancy when requested by enterprise customers. Solutions include path protection, such as the availability of back-up fiber, along with OLT and ONT equipment redundancy and combinations of these approaches.

Growing Ecosystem and increasing diversity

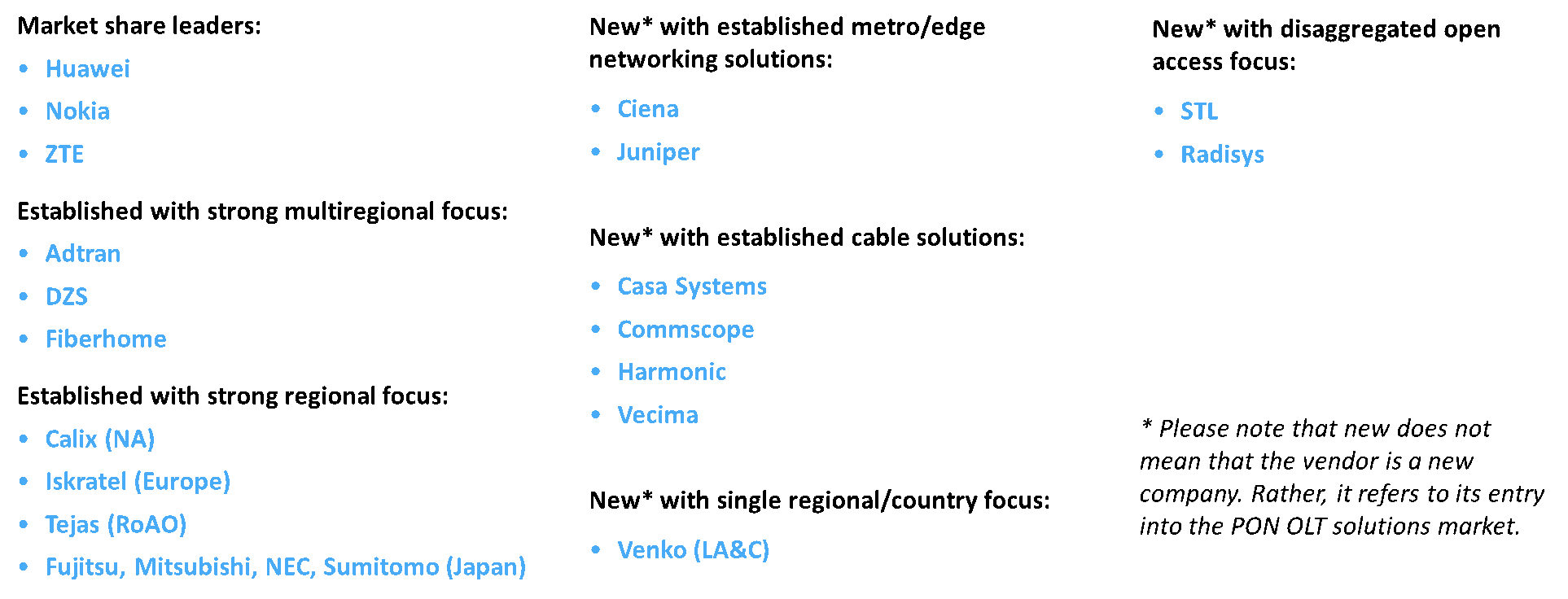

The strong growth in the PON equipment market, and the use of PON by different types of CSPs and enterprises, are attracting new suppliers; consequently, the PON OLT vendor market is expanding. An overview of the PON OLT vendor landscape is shown in Figure 4.

New vendors reflect several key trends that are being adopted by some CSPs, including:

- Merging of access and metro networking equipment

- Movement toward disaggregation and open access

- Addition of FTTP by cable network operators

As PON and next-gen PON deployments grow across the globe, different solutions are needed to meet operator and enterprise requirements. OLT solutions vary by:

- Capacity, such as line-card or port count

- Physical location, such as indoor, edge, or remote field-based

- Standalone equipment or add-on to existing equipment, such as pluggable OLTs for cable digital nodes or switches/routers

- Combo PON with support for 10G GPON and GPON versus non-combo

- Support for beyond 10G, such as 25G PON and 50G PON

CSPs should embrace the growing field of vendors, offering solutions that fit specific FTTP network goals and strategies. Some solutions fit extensive overbuild strategies, while others focus on selected buildouts. With the introduction of 10G, 25G, and 50G PON, network operators have a wider range of options for meeting bandwidth growth along with the use of PON for nonresidential customers and applications.

Summary

PON-based fiber access is growing around the globe leading to new, significant opportunities for PON equipment and component vendors. Vendors must select the opportunities that best fit their respective technology and solution strengths, and work closely with customers and prospects to improve the selection process and outcomes. Component vendors must work closely with the ecosystem too, and pick the opportunities that best fit their capabilities and business models.

The PON component and equipment market is in the “WoW” stage. Omdia welcomes meetings with the ecosystem during OFC 2023.

Julie Kunstler, Chief Analyst, Broadband Access Intelligence Service

askananalyst@omdia.com

Citation Policy

Request external citation and usage of Omdia research and data via citations@omdia.com.

Copyright notice and disclaimer

The Omdia research, data and information referenced herein (the “Omdia Materials”) are the copyrighted property of Informa Tech and its subsidiaries or affiliates (together “Informa Tech”) or its third party data providers and represent data, research, opinions, or viewpoints published by Informa Tech, and are not representations of fact.

The Omdia Materials reflect information and opinions from the original publication date and not from the date of this document. The information and opinions expressed in the Omdia Materials are subject to change without notice and Informa Tech does not have any duty or responsibility to update the Omdia Materials or this publication as a result.

Omdia Materials are delivered on an “as-is” and “as-available” basis. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information, opinions, and conclusions contained in Omdia Materials.

To the maximum extent permitted by law, Informa Tech and its affiliates, officers, directors, employees, agents, and third party data providers disclaim any liability (including, without limitation, any liability arising from fault or negligence) as to the accuracy or completeness or use of the Omdia Materials. Informa Tech will not, under any circumstance whatsoever, be liable for any trading, investment, commercial, or other decisions based on or made in reliance of the Omdia Materials.

Omdia Materials.

Posted: 6 January 2023 by

Julie Kunstler, Chief Analyst, Broadband Access Intelligence Service

| with 0 comments