By Woo Jin Ho, Analyst - Semiconductors and Comms Equipment, Bloomberg Intelligence

The annual Optical Fiber Conference (OFC) has grown in importance for the financial community due to the increasing use of high-speed optics with hyperscale cloud providers and telecom providers. Optical systems, component and chip makers have used OFC as the platform to make key technology announcements, and OFC 2020 should be no different. While our blog post focuses on the emergence of 800G technologies, other areas of interest for the financial community include 400ZR and silicon photonics, as well as market consolidation and progress on the 5G and fiber deep roll outs. This blog post is based on a Bloomberg Intelligence report published on Bloomberg terminal.

Investors Focused on Ciena, Infinera 800G Dash

Among the areas of focus for investors attending the annual optical fiber conference (OFC) in March the race to 800 gigabit optics. Investors will be tuned-in on Ciena’s and Infinera’s 800G timelines and developments, with products ramping up this year and next. Based on earnings results comments, Ciena should be first to market with WaveLogic 5 800G in early 2020, which is expected to deliver meaningful revenue in 2H20. Infinera should follow with the delivery of its 800G ICE 6 chip solution sometime in 2H20.

A lot may be at stake for the two companies with their respective 800G launches. For Ciena, it will aim to keep its technology and competitive lead in transport and data center optics in order extend its market leadership. In contrast, Infinera will aim to leverage 800G as one of the engines to close the technology gap and get back on track financially.

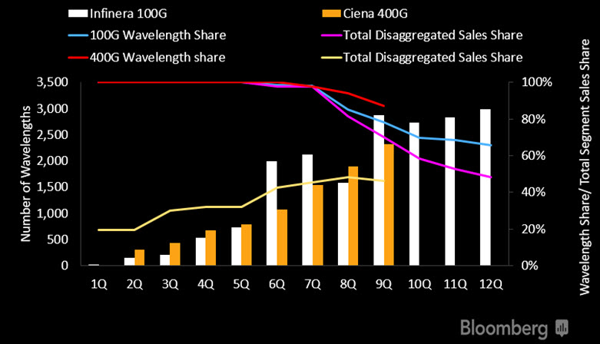

Mainly A Cloud Audience In Early Days

800G optics will not be cheap when it first launches, and the high costs will limit the audience to hyperscale customers. But costs aside, the applicability of 800G at full capacity limits the technology adoption to hyperscale cloud customers for data center applications. This scenario is similar to early days of the 400G launch. Ciena was first to launch 400G optics in 4Q17. According to Dell ‘Oro, nearly 1,900 400G wavelengths shipped in the first four quarters, of which 74% were purchased for data center interconnect applications, mainly to internet cloud providers (ICPs). We expect the early days of 800G optics to plot a similar path toward the cloud. This bodes well for the first movers, since ICPs have been investing aggressively to grow capacity and fueled the underlying growth in the segment.

Chart: Disaggregated Optical 100/400G Wavelength Share (from Initial Launch)

Source: Dell ‘Oro, Bloomberg Intelligence

800G Is More Than Speed, Eventually More Than ICP

The applicability of 800G optics may quickly expand beyond ICPs and could quickly expand to telecom applications for the transport and submarine networks. 800G will be the headline metric for most investors. But focusing on the speed metric is too narrow in scope, since 800G transponders can be tuned to slower rates for further reach. The ability leverage 800G for longer distances could spark telecom customer interest for metro, long-haul applications. While telecom’s rate of optical spending growth is slower than cloud spending, it’s still the larger portion of overall optical spending and typically come with higher margins than cloud deals.

The timing of 800G technology corresponds with key emerging network trends for the telecom sector, such as 5G wireless, fiber deep and high capacity long haul and regional metro deployments.

600G Can Co-Exist in 800G Ramp Up

The emergence of 800G optics shouldn’t diminish the recent 600G product introductions since customers seek vendor options. Optical networking is not a one-sized fit all, and customers will seek products that best fit their network architecture, while driving favorable economics. The initial 800G vendor list is short – Ciena and Infinera. Even if additional vendors make 800G announcements at OFC, these two vendors should still have at least a 1-year lead over new entrants, which would limit the vendor diversity that customers prefer.

600G merchant optics, such as those from Acacia and NEL, can offer a viable alternative for customers, and help broaden the narrow 800G vendor field. While capacity matters given the burgeoning data consumption growth, it won’t come at any cost. Ultimately, network providers will aim to bring down the cost per bit economics to maximize the return on network investments.

Posted: 21 February 2020 by

Woo Jin Ho, Analyst - Semiconductors and Comms Equipment, Bloomberg Intelligence

| with 0 comments